Powering Southeast Asia’s charge to a sustainable future

Credits

Analysts

Mr Ang Wei Xuan, Summer Analyst

Research

Mr James Tan

Overview

The world’s population reached 7.9 billion in 2021. Its resources are already being pushed to the brink, and we are facing unprecedented social inequalities, environmental degradation, and governance issues.

Without taking the necessary steps to mitigate these effects, we are poised to see temperatures rise by 1.5 to 2ºC by 2050. The resultant detrimental effects, including a large increase in the frequency and scale of natural disasters, spread of diseases and ecosystem disruption will make life untenable for many regions, including Southeast Asia.[1] This will derail the lives of millions, and it would not be unfair to say that how governments, corporations & communities come together to tackle this mammoth problem will define the lives of many generations to come.

The severity and urgency of the problem has seen hitherto silent stakeholders begin taking action to ensure sustainability on all fronts. In this regard, we believe that early stage venture capital can serve a crucial role in resolving critical problems by financing and developing innovative tech-based solutions. The dual goals of profit and impact allow leveraging of market forces to scale quickly and effectively. This report aims to provide an insight into the ongoing sustainability efforts, trends and outline the reasons for our bullish sentiments towards sustainability-focused investing.

Foreword

Mr James Tan

Managing Partner

Quest Ventures

The ‘take-make-waste’ industrial model is no longer feasible. With a larger GDP than the rest of the world combined, and as the fastest growing economic region, what Asia does as it rises will have a significant impact.

With a trillion dollars in economic benefits if efforts to go green in Asia go right, and climate change and other disastrous effects if the efforts do not, the stakes are high.

We believe that governments need to push for sustainable practices on a national, regional and international level.

We believe that businesses must align between sustainability and corporate gains. Old and new businesses alike must commit to incorporating ESG goals in their key decision making.

We believe that the financial services industry can encourage industries to implement ESG criteria into their decision making, as well as rewarding efforts made towards sustainable development.

Time is not on our side. Our three tenets are merely a starting point. Governments, corporations, and individuals that want to do more can count on increasing awareness and support globally to drive changes. We look forward to working with them towards a sustainable future.

Defining Sustainability

The 1987 United Nations Brundtland Commission’ defined sustainability as the goal of “meeting the needs of the present without compromising the ability of future generations to meet their own needs. Today, sustainability is inevitably centered around environmental issues. However, we must keep in mind that sustainability also encompasses social issues like inequality, as well as economic issues such as trade, and that all these issues are often intertwined.

Since the Industrial Revolution, the onset of capitalism and the industrial economic model has seen humanity consume resources at an unprecedented rate. Conservation of the environment was but an afterthought as natural resources were exploited for economic growth. Modern superpowers such as the USA and various European countries built their success on the back of the deployment of large quantities of less efficient technology, powered by finite natural resources. That has already caused irreversible damage to the ecosystem, creating issues such as global warming, extreme weather events and environmental degradation.

As of June 2021, the world population has reached approximately 7.9 billion. Sustaining so many on the old ‘take-make-waste’ industrial model is no longer feasible, and will only exacerbate the harm to our planet. We need to find ways to make more from less, focusing on social and environmental outcomes instead of economic ones.

However, it is a tremendously unfair request from the Western developed countries (NOA, EUR) for countries in developing regions (APAC (including SSEA and EAS), MENA, LAC, SSA) to forgo the same tools and methods that had worked so well for them in their pursuit of economic development.

As such, an integral determinant to the success of the sustainability push is how developing regions incorporate sustainable development as they rise.

Of particular importance will be Asia’s approach. Asia is the fastest growing economic region today, with a larger GDP than the rest of the world combined, both in nominal and PPP (Purchasing Power Parity) terms. By 2030, Asia will be home to 60% of global growth and 4.9 billion people.[2] While China, Japan and South Korea are already global leaders in green technology, how the rest of Asia adapts will become of paramount importance to the global fight for sustainability.

The physical effects of unsustainable growth, combined with growing research in and awareness of climate science & environmental issues have pushed sustainability to the forefront of the collective human consciousness, where it had once lingered at the back of for years. People today know that the fundamentals underpinning economic growth must change.

The UN has contributed towards pushing for global cooperation in this regard, and the well-known Sustainable Development Goals (SDGs) spur ambitious targets for companies, countries and individuals. Reaching them can only be achieved via sustainable practices. This can be defined as generating positive value for stakeholders, or not harming them at minimum, and improving environmental, social and governance (ESG) performance in areas where one has an impact.[3] However, the increase in adoption of sustainable practices by countries and corporations in recent years has its roots not just in lofty aspirations, but also in more practical reasons.

Governance Case for Sustainability

Traditionally, governments have avoided pursuing an overt sustainability agenda. While Bhutan has achieved carbon negative status, it did so at the expense of economic growth; few developing countries are willing to make that tradeoff.[4] Sustainability seemed to be a luxury only wealthy countries could afford.

However, in the face of worsening climate risks, developing Asian governments have become increasingly aware that they can no longer afford to focus exclusively on economic growth and leave sustainability for later. They have to achieve both in tandem, or risk facing larger problems in the future.

High Stakes & Strong Motivations

Asia, and to a large extent Southeast Asia (SEA), is particularly vulnerable to climate change, due to the concentration of economic activity and population along coastlines and the reliance on agriculture, forestry & natural resources for livelihoods. Rising temperatures, sea levels, increased frequency of natural disasters (floods, cyclones, heat waves) and decreasing rainfall are effects that governments cannot afford to sit back and ignore. The rapid onset of pollution and degradation has had far-reaching consequences on the standards of living for citizens in Asian countries. Studies have also shown that deforestation and climate change increase the risk of zoonotic disease transmission (such as COVID-19). Becoming more sustainable has become a key socio-political promise for governments, with good reason.

In the absence of appropriate adaptation and mitigation measures, McKinsey predicts that by 2050, up to $4.7 trillion of GDP in Asia will be at risk annually due to increased heat and humidity causing a loss of effective outdoor working hours.[5] It has also been predicted that by 2050, the exacerbation of natural disasters could cause $1.2 trillion of damage to capital stock from flooding in any given year and cause up to 40% of land area to experience shifts in biomes, affecting ecosystems and livelihoods. These effects have been corroborated by independent research done by the Asian Development Bank (ADB), which projects a decline of up to 50% rice yield potential and 6.7% combined GDP each year by 2100.[6]

Significant Potential Upside

On the other hand, Asian and South-East Asian economies have much to gain by focusing on greening their economy. A report by Bain claims that SEA could see up to US$1 trillion in economic benefits up for grabs by 2030 if it successfully builds a green economy and becomes a more attractive investment destination. [7]

Research done by think tanks ClimateWorks and Vivid Economics posit that a low-carbon industrial strategy could be the golden opportunity for ASEAN to recover from COVID-19.[8] They argue that ASEAN member countries are uniquely positioned, being both in close physical proximity as well as possessing strong existing trade relations with China, Korea and Japan, the current leaders in low-carbon technology. Combined with lower wage structures, improving infrastructure and a supportive legal environment, ASEAN is an attractive prospect for the leaders looking to scale up production and build more resilient supply chains. This opportunity for technology and expertise transfer for ASEAN countries to restructure their own economies while providing sustainable jobs for the economy.

Business Case for Sustainability

Thankfully, the policymaker’s viewpoint is shared by the corporate world. Leading management consulting firms such as Accenture and McKinsey have argued that sustainability and the circular economy represent the greatest business opportunity in over 100 years.[9] Traditionally, ESG goals were only pursued by companies on the basis that it coincided with their business philosophy or core values. Today, ESG goals are pursued because the double bottom line has been proven to be achievable, and there are tangible benefits to proactively integrating sustainable practices into one’s business strategy.

Managing Risks

Supply chains have a history of being affected by events outside any company’s control. Resource depletion and degradation of natural capital assets have the potential to rack up staggering losses for overly dependent corporations. By investing in the appropriate green technology and pivoting to more sustainable practices, corporations can reduce their vulnerability to resource scarcity and supply chain disruptions, but also avoid potentially having stranded assets.

Bolster Performance

A summary of 200 studies investigating the link between corporate performance and ESG goals done by the University of Oxford and Arabesque has posited that good ESG performance positively correlates to better stock price performance, operational performance and lower cost of capital in more than 80% of all cases. [10]

Mounting Investor Expectations

While ESG reporting is not a new phenomenon, it has only been in recent years that institutional investors have pushed for greater accountability of companies with regard to ESG challenges. This is in line with greater civic consciousness and expectations for companies to step up and contribute to solving issues like income inequality, climate change etc.

The 2020 EY Global Institutional Investor Survey of nearly 300 institutional investors shows that 91% used non-financial performance as a pivotal consideration in investment decision-making, and investors are set to consider it even more rigorously as the links between ESG performance and financial performance become clearer.[11] Despite the setbacks of the COVID-19 pandemic, investors have not reverted to short-term performance models. Rather, it has cemented the importance of long term resilience and the crucial role ESG performance plays in achieving that. Investors are also holding companies accountable, and those that fail to meet expectations risk losing precious access to capital markets.

The wealth transfer to the younger generation has also seen a shift in investing philosophies, with surveys showing that Millennial respondents are more committed towards achieving social impact and long-term value creation with their investments than simple financial gains.[12]

Larry Fink, CEO of Blackrock, has testified to the shift in client priorities towards climate change and sustainability agendas, most recently in his 2021 letter to CEOs.[13] This is a reflection of the growing number of institutional investors, not just Blackrock, that are demanding both greater reporting and moving their investments towards sustainability-focused companies.

Companies looking to navigate through the changing financial services landscape will have to adapt to mounting pressure from investors with regards to sustainability.

Mounting Consumer Expectations

In the past, consumers had previously balked at paying extra for sustainable products, and companies with sustainable products at higher prices were typically doomed to failure. However, changing consumer trends, spurred in part by the coming of age of the environmentally & socially-conscious millennials/Gen Zs and enabled by increasing levels of wealth in a post-recession world, have fuelled an increase in the demand for products whose brands display evidence of corporate social responsibility, sustainability and respect for others.

Recent empirical research strongly supports the existence of ‘shared value’, the proposition that companies can do well by doing good.[14] This offers companies the opportunity to build new global brands specialising in green products and surpassing large incumbent competitors. For example, EV companies have the opportunity to upstage traditional car manufacturers as trends change.

According to the Harvard Business Review, companies can even charge up to 20% price premiums based on positive corporate responsibility practices.[15] This strong customer motivation to support sustainability further shows itself in the form of consumer support for a range of trustworthy sustainable products & services, creating superior revenue growth channels for companies. [16]

Achievable Double Bottom Line

Corroboration by multiple sources and the cumulative efforts of research done over the years has made it apparent that the double bottom line is no longer imaginary. A pivot to sustainability is as inevitable as it is necessary. The earlier companies recognise and make efforts to reposition themselves, the better poised they will be to ride through the green revolution. We can expect that as the business case becomes more apparent to top management, sustainability will be adopted at an increasing pace.

Categorising Businesses Based On Their Approach to Sustainability

Today, we can categorise businesses into 4 main categories based on their approach to sustainability.[17] Out of these four, three types are receptive towards ESG goals, namely:

1. Businesses in industries with traditionally unsustainable supply or value chains, but are committed to pivoting towards environmentally friendly processes and products. Examples include those in the automotive industry that are making the switch to EVs or those in the consumer electronics industry that are considering social issues such as minimum wages, living standards and conservation of resources/recycling.

2. Businesses that disrupted older business models and brought about positive ESG-related impact as a byproduct. Examples include ride-sharing companies such as GoJek, Uber, Lyft, Grab that have reduced the need for everyone to purchase a car by making ‘private’ transport ubiquitous and cheap, conserving the resources associated with car production and ownership. In Singapore, BlueSG is pioneering accessible EV rental. Airbnb has minimised hotel wastages by capitalizing on spare bedroom capacity globally.

3. Businesses that are driven by sustainability from the onset. This includes any form of social enterprise or primarily impact-focused businesses. Internationally, examples include Unilever and Novelis.

The last type of businesses however are standing in the way of widespread adoption of sustainability. This group comprises of:

4. Large businesses in legacy/sunset industries such as those in coal, gas or petrochemicals, that still have significant political/lobbying influence where they are based.

Three Tenets For Sustainability

Growing awareness within the public and private sectors of the perils of feckless and unrestrained industrialisation has prompted increased attention to the subject of sustainability. It is heartening to see that all UN member states have signed commitments to the UN’s Sustainable Development Goals (SDGs), and companies are making visible efforts to achieve sustainable milestones. Regionally, we are also seeing increased attention and support by blocs such as the EU and ASEAN, and there have been many other international agreements in pursuit of sustainability goals, such as the Paris Agreement, the Sendai Framework for Disaster Risk Reduction, the New Urban Agenda etc.

To bring the quest for sustainability to the next level, we believe that there are three mutually reinforcing keys that need to be employed in tandem.

Firstly, there needs to be support from the respective governments to push for sustainable practices on a national, regional and international level.

Secondly, businesses must become increasingly aware of the ever-growing alignment between sustainability and corporate gains. This can be achieved in two tranches. Existing businesses need to be convinced of the positive correlation, and subsequently commit to re-pivoting & incorporating ESG goals into their key decision making. Additionally, new sustainable impact-focused businesses must be given the opportunity to grow, provided that they meet critical criteria for success, both in terms of impact and in terms of profitability.

Lastly, the financial services industry needs to accomplish the dual roles of pressuring industries to implement ESG criteria into their decision making, as well as enabling and rewarding efforts made towards sustainable development. This will be crucial in pushing industries towards the tipping point.[18]

Quest Ventures is a long-standing believer in the business case for sustainability. In our 2020 publication done in collaboration with INSEAD MBA, we firmly stated our belief that business and ESG impacts are not mutually exclusive.[19]

While most demonstrated success has been in tech-related startups in Indonesia, Quest Ventures today is actively searching for start-ups with impactful value propositions and solid business models, operating within SEA, across a range of verticals. In our opinion, technology is key to ensuring that sustainability is synonymous with growth.

We have high hopes for the SEA region in particular, as there is notable progress being made towards unlocking the region’s sustainability. In this report, we will also be discussing Asia’s potential, how close it is to realising that potential and where we expect to see the largest developments in sustainability unfold.

The First Tenet: Governments

Private Sectors Follow The Government’s Lead

The business environment in Asia has historically been strongly intertwined with government prerogatives and the public sector. Governments provide the necessary support and confidence for businesses looking to test new waters, and their commitment provides strong impetus for the private sector.

This is exemplified by the Singapore government’s approach to building ecosystems within the economy, such as the start-up ecosystem back in 2015.[20] This ranged from broader policies such as positioning itself as a launchpad into SEA and a general openness to foreign talent and investment, the long-term commitment to the end-goal and vision for the local start-up scene to smaller details such as the fostering of a close community within a start-up hub (Block 71 in Ayer Rajah, JTC Launchpad), the nurturing human capital (the NUS Overseas Colleges (NOC) programme, SMU’s Institute of Innovation and Entrepreneurship (IIE) etc.) and capital investments (indirectly) through Temasek Holdings. It is clear that when governments are onboard and committed to certain agendas, there will be sufficient traction to overcome inaction and uncertainty in the private sector.

Another case study would be the importance of government initiatives in promoting the uptake of green technology. Globally, early attempts to introduce electric vehicles to the markets failed to make headways. Alongside improving technology and lower costs, electric vehicles have finally managed to take off, but only after governments stepped in with additional initiatives to supplement the manufacturers’ best efforts. These include CO2 emissions regulation schemes (e.g. in China, EU, California), efforts to expand the charging infrastructure in countries and subsidies to make EVs viable and competitive options against vehicles with internal combustion engines.[21] It is clear that the EV market would not have developed to where it is today if governments had taken the backseat. In Singapore’s Green Plan 2030, it intends to double the number of EV charging points to 60,000 by 2030, and gradually phase out internal combustion engines. It has also tightened the various vehicle emissions schemes in a bid to shift consumers to hybrid and electric vehicles. This marks the first of many ASEAN countries’ attempts to shift the citizenry towards EVs, where there has been little to no mainstream adoption before.

In this regard, governmental buy-in is an essential first step for convincing businesses and individuals to come aboard. Likewise, when it comes to ensuring a concerted push for sustainability across sectors, governments must lead the way, in order for this to be implemented into business strategies and personal actions.

While the COVID-19 crisis has had a devastating impact, it has also provided the opportunity for countries to restructure and rebuild back greener. In this regard, Europe leads the rest of the world in its efforts to resurrect itself as a greener economy. In the next few years, billions of dollars will flow into infrastructure and business investments across Southeast Asia and the entire Asian continent as well, and this opportunity needs to be grasped to strike a proper balance between social & environmental capital and economic outcomes, as discussed briefly earlier.

Questions Over Commitment

However, some remain skeptical of the prospects, pointing to studies showing that governments have been split with regards to their approach. An ING report offers the following analysis of several APAC/SEA countries and their Environmental Performance Indicator and green spending as a percentage of total Covid-19 stimulus. There is a clear discrepancy between countries like Singapore and countries like the Philippines and Indonesia.

Additionally, some point to certain indicators within Asia-centric measuring indexes, such as the Hinrich Foundation Sustainable Trade Index (STI) that allows us to get a more in-depth analysis of 19 Asian economies and how they fare in terms of sustainability across 3 factors: economy, environment and society.[23]

Taking a closer look at Indonesia, we see progress being made with regards to labor standards and educational attainment, and it has also increased factors like financial sector depth and technological innovation while reducing trade in natural resources.[24] However, Indonesia continues to do poorly in terms of environmental factors such as transfer emissions and air pollution.

Meanwhile, Vietnam regressed relative to other Asian economies in terms of social and environmental sustainability, showing declining labor standards and a lack of improvement in environmental considerations relative to 2018. [25]

Furthermore, some point towards ASEAN’s lackluster performance with regards to reaching its 2030 Sustainable Development Goals, where it continues to poorly perform with regards to environmental sustainability despite having made significant progress on socio-economic fronts.[26]

Cause for Optimism

Nevertheless, we are optimistic that Asia and ASEAN will still be able to build back post-COVID, more sustainably than ever, due to several mitigating factors.

Firstly, as the ING report rightly acknowledges, several countries are progressing on a “background of general environmental progress”.[27] It is also important to note that sustainability goes beyond environmental performance, and that we are looking for more than government spending, but the development of an environment that encourages private sector attention and adoption of sustainability on a national and regional scale.

Secondly, we cannot focus solely on negative aspects highlighted in the STI. While some countries have consistently done well on the STI, such as South Korea and Japan, others are still making good progress in other areas.[28] For example, China has made significant progress in reducing air pollution, while Pakistan reduced its deforestation considerably. Indonesia, Myanmar and Laos managed to diversify their trade bases away from natural resources, and Singapore also managed to reduce air/water pollution while implementing carbon pricing and lowering transfer emissions (pointing towards cleaner export industries).

This leads us to the conclusion that there is still progress being made overall, bearing in mind that the STI ranks economies relative to one another based on current achievements, and uses that as a proxy to measure progress towards meeting the Sustainable Development Goals. A low ranking does not necessarily mean that nothing is being done in any particular regard. In fact, we are witnessing pivots to sustainability in many countries that might require several years to bear fruit. The existence of the STI serves to continually suggest areas for improvement for both the public and private sector to come in and plug the gaps, and should not be taken as a pessimistic outlook for the region. Rather, the existence of such academically rigorous comparisons indicate that sustainability on all fronts is being taken increasingly seriously, and play an important role in encouraging the various governments to do better.

In fact, encouraging development has always been brewing in Asian countries. To provide some balance to the earlier discussion, it is important to note what countries like Vietnam, Indonesia, Singapore and even China have been doing with regards to meeting the SDGs.

Vietnam managed to move from being one of the poorest countries in the 1980s-1990s, to lower middle-income status by the 2010s, while keeping the SDGs in sight, and even presented a National Report on Sustainable Development at the UN Conference on Sustainable Development (RIO+20) in 2012 and a Voluntary National Review of its progress towards the SDGs in 2018. [29,30]

Vietnam continues to incorporate SDGs into its national development strategy, such as its previous 2011-2020 Social and Economic Development Strategy (SEDS) and 2016-2020 Social and Economic Development Plan (SEDP), and upcoming 2021-2030 SEDS and 2021-2025 SEDP.[31] The government has also done good work in encouraging sustainable practices and investments in the private sector, with initiatives such as the setting up of the Vietnam Business Council for Sustainable Development (VBCSD) and the creation of an enabling legal environment.[32] A more detailed report of Vietnam’s development and SDG progress is available from the IMF.[33]

It is also crucial to note Vietnam’s track record of efficiency with regards to adopting sustainable practices. This is shown through their achievement of installing 5 gigawatts (GW) of solar energy by 2020, exceeding their 1GW goal.[34] This also highlights the ability of Southeast Asian countries to execute plans quickly and effectively, bolstering our confidence in the region’s prospects. With Vietnam being Asia’s top performing economy through the pandemic, it is not a stretch to say that sustainable development will find its way into the government’s priorities again soon, and that this run of poor form is but a blip on an otherwise stellar trajectory. [35]

We also saw Indonesia launch its first sustainable development plan, the RPJMN 2020-2024 in January 2020. Research done by the Ministry of National Development Planning in collaboration with the World Resources Institute found that sustainable, inclusive growth could “deliver average GDP growth of 6 percent per year through 2045 and, compared to business as usual, create more than 15 million additional greener and better-paying jobs, halve extreme poverty, and save 40,000 lives annually from reduced air and water pollution – all while reducing greenhouse gas emissions by nearly 43 percent by 2030, exceeding Indonesia’s current international target.”[36] Buoyed by the prospects, Indonesian policymakers are doubling down on efforts to roll out low carbon development initiatives, and we believe that Indonesia stands a good chance of success with the scale of their efforts.

In Singapore, the government also continues to push for greater sustainability across all sectors of the industry, having recently unveiled the Singapore Green Plan 2030.[37] This is a comprehensive plan that aims to garner buy-in from the citizenry and private businesses through initiatives including, but not limited to, the Eco Stewardship programme, greening of resource-intensive industries such as the petrochemicals industry, and the Enterprise Sustainability Programme to support local enterprises to adopt sustainable practices and seize opportunities in the sector. Singapore intends to position itself as a sustainability solutions hub, offering tech solutions for water treatment, upcycling, urban farming, decarbonization etc. There is also awareness that sustainable technology in areas such as agriculture can be used to further other goals, such as Singapore’s ‘30 by 30’ food self-sufficiency.

We remain optimistic that individual member states of ASEAN recognise the importance of sustainability, and that armed with the data from research and the growing technology available, they will be able to tackle the various issues that have drawn attention from detractors. As a regional entity, we believe ASEAN will continue to play a formative role in promoting sustainability by providing the right environment for growth. This includes, but is not limited to: regional cooperation, laying out regional standards for sustainable finance and monitoring sustainability efforts.

On a larger scale, we have seen Asian countries make significant pledges to meet the Paris Agreement’s goals. A large number of these initiatives revolve around achieving carbon neutrality, adopting new energy sources or reducing the emissions intensity of GDP. [38] It is inevitable that governments will have to step in and provide the necessary carrots and sticks to attain these goals.

The Second Tenet: Businesses

Becoming Aware Of The Business Case

While the business case for sustainability constitutes an indisputable fact, sustainability cannot succeed if corporations and businesses do not acknowledge or implement strategies according to it. Presently, the business case is catching on quickly via two methods.

The first method is organic, as management becomes self-aware of the impacts caused by both the supply chain and value chain. This can come about through generational power transfers, as existing businesses hand over management responsibilities to a younger generation of CEOs. A study of young CEOs in China proved that they are more conscious about their ESG footprint and have higher tendencies to adopt sustainable practices within their companies (Shahab, Ntim 2019).[39]

The second method is through third-party pressures strong enough to overcome entrenched resistance. In this approach, there are some overlaps with the business case, such as investors and consumers demanding greater accountability and moving towards more sustainability-focused companies.

Internally, throughout the corporate ladder, employees are becoming increasingly vocal about value-alignment with the company they are working with. When it comes to hiring and retaining top tier talent from the millennial generation, a survey showed that nearly 40% decided between jobs based on the company’s sustainability performance, while almost 70% of respondents said that a company’s sustainability plans would influence their long-term decision to stay.[34] Performance indicators and employee happiness also increase when employees think what they are doing has meaning.This complements a large body of research that points to the growing phenomenon of workers choosing value creation over wealth generation.[41] Ultimately, the speed and efficacy will depend on the willpower and action of various stakeholders mentioned above.

For the companies that have caught on to the winds of change, there are several essential steps that can be taken to prepare their company.

First, corporations should conduct an honest appraisal of their current business practices and environment. This will involve examining the industry they operate in, their supply chain, as well as their value chain to note the impacts that their product/production processes are generating.

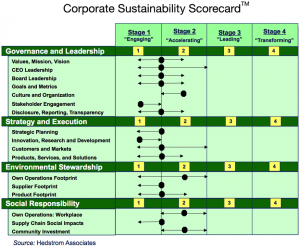

There are many available scoring systems that companies can choose to use, one such system being Hedstrom Associates’ proprietary Corporate Sustainability Scorecard.[42] In short, this evaluates a company’s sustainability efforts in terms of 4 key aspects: Governance and Leadership, Strategy and Execution, Environmental Stewardship and Social Responsibility. Each section had 17 elements and 8-12 sub-elements, totalling about 150 Key Sustainability Indicators (KSI). A thorough evaluation will allow management to determine how far along the company is on the path to sustainability, how they compare to peers and competitors, and what the best practices today are. This will pave the way forwards with regards to the next steps that the company should be taking.

With regards to environmental stewardship, a common ideal for businesses across industries should be the attainment of a circular economy. This refers to an economy where waste and pollution is reduced, products and materials are reused & recycled and natural resources are regenerated. This concept applies across the supply chain and the value chain, so we will briefly cover some of the general aspirations.[44]

Reduction: This can be defined very broadly to encompass a variety of processes. Constraining ourselves to the supply chain, there are several ‘reductions’ that companies should aim for.

One of them is to reduce the negative externalities created during production. For example, aiming for carbon neutrality is a fine goal for those in the manufacturing line, and beverage companies such as the Coca-Cola Company might pursue water neutrality. Additionally, companies should seek to reduce the amount of raw materials necessary, especially if the process of obtaining said materials endangers the environment (mining, logging). This amounts to a need for innovation, both to discover alternatives and to discover more efficient ways of production.

With regards to the value chain, reduction is typically done by consumers, by being more mindful of their consumption and not to be as wasteful. On the companies’ end, we prefer to term their efforts in reducing waste as reusing and recycling.

Reuse & Recycling: Companies should try to recover and recollect used consumer goods or byproducts from the production process, and reuse or recycle them for other purposes. This is especially pertinent when it comes to plastic products, which do not biodegrade in landfills, or for rare metals used to produce electronics and are already in scarce supply. By lengthening the lifespan of each material, we will need to use less in the long run.

Regeneration: Companies that have no choice but to use natural resources such as timber should be proactive in the regeneration of forests. Switching to renewable resources (such as solar power as opposed to fossil fuels) for certain processes will also go a long way in stretching the lifespan of the finite resources we have left. In fact, they should be prioritised and implemented where possible.

When it comes to social responsibility, all corporations, regardless of the scale of their operations, have the bare minimum responsibility of making sure that their business activities do not infringe or compromise on the quality of life for local communities, diminish their dignity or threaten their way of life. The best practice for corporations would be to rise while simultaneously uplifting the community that they are based in. This could be through providing fairly compensated employment, providing sufficient employment benefits, bearing the cost of building shared infrastructure (e.g. roads) or supporting the community through various other means. Companies should be going beyond the bare minimum stipulated by the law. Even in the absence of proper regulation, companies should be mindful and aware of these issues, not just out of compassion but also to not draw the ire of the public eye, as Apple, Nike and Volvo have learnt the hard way.

By virtue of their size and the value of the foreign direct investment they represent to developing countries, large corporations have the power to make certain prerequisites before committing to a new plant or factory in developing countries. This gives them the opportunity to make positive change, such as pushing governments to incorporate proper labour laws, safety regulations and requirements in order to become more attractive. Companies should not exploit the lack of such governance, but rather set the precedent and industry standards where possible.

Second, businesses need to engage in greater sustainability reporting. In some cases, certain metrics are not being measured at all, and in other cases, the impacts are not fully investigated. Where possible, corporations should continuously seek to implement new technology that allows for accurate tracking, diagnosis and reduction of detrimental impacts.

Instead of having to retroactively modify old policies, start-ups might find it easier to embed ESG policies into their fresher business practices. On the other hand, startups might also be pioneering new concepts and technology that already have a sustainability-related value proposition.

Regardless, the key for businesses is to possess a management both aware of the risks ahead and committed to contributing to sustainable development. We can thankfully count on the fast-changing financial services landscape to bolster these dual factors.

The Third Tenet: Finance

An Overview of Sustainable Finance

Sustainable finance, as defined by the Monetary Authority of Singapore (MAS), is “the practice of integrating environmental, social and governance (ESG) criteria into financial services to bring about sustainable development outcomes, including mitigating and adapting to the adverse effects of climate change.”[45] In addition, the European Commission states that “Sustainable finance also encompasses transparency when it comes to risks related to ESG factors that may have an impact on the financial system, and the mitigation of such risks through the appropriate governance of financial and corporate actors.”[46] In recent years, there has been growing understanding that businesses and governments will need the financial sector’s assistance in order to grasp the high-risk high-return opportunities associated with sustainability, and that the UN SDGs will be unobtainable without them.

This has opened the door for companies to issue financing instruments (sustainable bonds) for the specific purpose of environmental/social projects. These instruments include green bonds, social bonds and sustainability bonds, which must be exclusively used for projects that bring about positive environmental/social impact. These open new financing channels for companies to pivot successfully, or undertake new climate/environmental related projects.

Another class of financial instruments, Sustainability-Linked Bonds (SLBs), are bond instruments which tie the financial/structural characteristics according to whether the issuer achieves predefined sustainability KPIs or ESG objectives. This provides financial institutions with the opportunity to lay down industry-agnostic and industry-specific metrics for sustainability/ESG objectives. These have grown in number along with the development of measurement metrics for sustainability objectives, such as the Sustainability Accounting Standards Board’s Materiality Map.[47] As our understanding of important indicators develops, it becomes easier for investors to not only trust green investments, but also sift through and evaluate opportunities.

Movements in Asia by governments and financial institutions mean that these new classes of financial instruments are rapidly catching on. According to a Moody’s report, Asia Pacific issuers accounted for 24% of global dollar-denominated green bond issuance, up from 8% 5 years ago.[48]

As of 2019, the Asian Development Bank (ADB) has issued $7.9 billion worth of green bonds since its first issuance in 2015.[49] Nikkei Asia estimates that the Asian dollar-denominated green-bond market is now worth USD 50 Billion, and HSBC adds that despite the downturn caused by COVID-19, issuance will return to pre-pandemic levels in 2021.[50]

In March this year, J.P. Morgan led Asia (ex-Japan)’s first SLB, with a $200 million note for Hong Kong-based property developer New World Development (NWD).[51] This offering was hugely oversubscribed, and is reflective of a greater phenomenon in the sustainable finance sector, with demand for green bonds consistently outstripping supply (by almost 6x).

These new types of financial instruments have caught the eye of fund managers and Asian investors for several reasons.

Firstly, there is evidence that bond returns from green bonds are in line with returns generated from traditional financial instruments. This helps to allay concerns that expected returns will be compromised for the sake of particular agendas. Another draw is that Asian green bonds remain priced consistently with conventional bonds, whereas in Europe investors would have to pay an 9 basis-point price premium on average for holding European green bonds. The homogeneity between asset classes has contributed to the positive reception in Asia.

Secondly, the governments of regional powers have moved to support the burgeoning investment sector. For example, the Monetary Authority of Singapore (MAS) has set up a sustainable bond grant scheme by subsidizing part of the costs incurred by first-time and repeat issuers, and has also set up a Green Finance Industry Taskforce (GFIT) to coordinate efforts in the space by banks, asset managers and issuers.[52] Japan has most recently issued its first government backed green bonds for environmentally friendly houses. Many Asian countries including China and ASEAN countries have also stepped up by publishing green guidelines and frameworks for the financial services industry. Regionally, we have also seen the ASEAN Green Bonds Standards being established, and China’s publication of the Green Bond Project Endorsed Catalogue of the People’s Republic of China.

Issuance in the first half of 2021 has already surpassed the record total in 2020. We expect to see the issuance of such bonds increase even further in the future, as governments provide the necessary support required to promote the issuance of such bonds in order to meet their carbon neutrality and sustainability goals, companies recognise the credibility green finance instruments provide to their brand image and investors increasingly include them in their portfolios.

Sustainable investing has also gotten increasing attention and acceptance from the financial services industry. It refers to the investment philosophy of achieving competitive (comparable relative to traditional investing methodologies) portfolio risk/return profiles while also achieving positive ESG effect. It’s rise is mainly due to the rising pervasiveness of values-based and performance-based mindsets. The former refers to genuine concern about the long-term health of the environment and society, while the latter refers to the acknowledgement of the growth potential in ESG-related investments as well as the recognition of potential ESG risks and the need to mitigate them.

Sustainable investing encompasses a range of strategies that are each best suited to a particular class of investor. These strategies are best expressed via the diagram below, and we will go into more detail on several of these strategies below.

Institutional Investors

The UN Principles for Responsible Investment give us a succinct summary of the roles institutional investors can play in pushing for ESG agendas in countries.

Institutional investors are more likely to engage in the ‘Avoid’ strategies, such as negative screening, in a bid to reduce their investments and/or support for unsustainable businesses.

This is an approach favored by banks, such as the Overseas Chinese Banking Corporation (OCBC), which has moved away from financing infrastructure reliant on fossil fuels, in favor of providing loans to build sustainable infrastructure such as wind and solar farms.[54] Such an approach has also been codified by the World Bank’s private lending vehicle, the International Finance Corporation (IFC), in their Green Equity Approach (GEA) aimed at eliminating coal financing within its portfolio.[55] More recently, the Asian Development Bank announced in May 2021 that it would no longer finance fossil fuel projects if other cost-effective technologies were viable alternatives.[56]

Furthermore, funds such as Blackrock, State Street, Vanguard & Temasek are leading the rest of the pack with regards to integrating sustainability into the active investment process and reducing exposure to sectors with heightened ESG risk.[57] Different financial groups in Asian countries are also gradually renouncing unsustainable investments, and incorporating climate risk into their assessments of investments.[58] In the coming years, we will definitely see more financial groups come under pressure from a multitude of stakeholders and eventually conform to the green standards set by supranational organizations such as the United Nations or ASEAN. As financial institutions walk away from short-term profit and overturning decades-old stances on highly resisted policies such as coal bans, it is inevitable that the next pockets of growth will reside in verticals that can best capitalise on new-found demand for green solutions.

Additionally, we have also seen institutional investors increasingly factor sustainability metrics and risks (eg. climate risks, transition risks, physical risks, long-term impacts on profitability) into their decision-making process. For example, asset/wealth managers like Blackrock, UBS, Citi and Blue Harbour Group are increasingly integrating proprietary ESG measurement tools to assess related risks, characteristics and signals of companies, with the goal of offering a suite of index funds and exchange-traded funds (ETFs).[59, 60, 61] With the influence that they have on management, large asset managers can show their support for certain management proposals and actions during the proxy voting season. For example, Blackrock has voted against management recommendations on more than 250 resolutions in 2021 compared to 53 resolutions in 2020, based on environmental considerations.[62]

These asset managers are also pushing for corporate sustainability reports to follow sector-specific standards, frameworks & regulation, which would make it easier to conduct research, make comparisons and allocate capital.[63] A UBS survey of over 100 asset managers also showed almost 75% of asset managers were intending to vote in favor of climate-related disclosures.[64] In Asia, ESG reporting is largely guided by voluntary reporting frameworks such as the GRI Standards.[65,66] However, we are also seeing convergence to common standards, with single standard discussions dominating events such as the Asia Sustainability Reporting Summit 2020.[67] In ASEAN, Singapore, Malaysia, Indonesia, Vietnam, Thailand and the Philippines all require some form of ESG disclosure and each government offers guidelines to issuers.[68, 69]

According to research done by Morningstar, there were 534 sustainable index mutual funds and exchange-traded funds globally, accounting for $250 billion as of June 30 2021.[70] This is not just due to funds pushing forward with their own beliefs about sustainability, but reflective of growing demand from individual investors and the trust in ESG-based assets to outperform the broader market.[71]

Institutional investors might also consider impact investing in the private markets as another way of achieving positive ESG effects. This can be done through direct equity investment in private companies (SMEs), or through investing in private equity (PE) funds or fund of funds (FoFs).

Impact Investing

Impact investing refers to capital placed into private equities in the hopes of generating ESG value alongside financial returns. This can take place across many different sectors and aim to achieve many different objectives, but the unifying themes are as follows.

Impact investors draw their faith from several underlying beliefs. Firstly, the historical success private businesses have shown in innovating and solving the problems of the day. Secondly, there are untapped financial opportunities to be found by focusing on overcoming the gaps between achieving ESG goals. This is termed as ‘base-of-the-pyramid investing’, where providing basic services to the poor offers large opportunities for SMEs to expand. Lastly, they also believe that greentech and sustainability is the next pocket of growth.

Some investors may choose to focus on capital preservation (‘impact first’), while others might be more focused on financial returns (‘financial first’). However, both are similar in that they seek a base-level of financial return as opposed to philanthropic grant giving. Detractors might say that impact investment is profiteering off others’ suffering, but studies have shown that this is a more efficient way of raising capital for those in need, and provides the right incentives to ensure that allocated capital brings long-term value as opposed to one-way grant allocation.[72]

The IFC has stated that private investments in SMEs is the top way of achieving maximum social impact on local economies.[73] This is due to the knock-on effects such as job creation, poverty reduction and economic development.

We echo this sentiment at Quest Ventures, and firmly believe that private equity investments are particularly powerful in emerging markets such as Southeast Asia. According to the Business & Sustainable Development Commission, a significant percentage (> 50%) of the SDGs’ business opportunities are in developing countries, and emerging markets constitute the biggest opportunities in the agritech, smart cities, cleantech, healthtech verticals.[74] Advancing impact investment in emerging markets could create more than USD 12 trillion in market opportunities and up to 380 million jobs by 2030, of which many would be in emerging market cities.

Finally, impact investors such as venture capitalists are uniquely positioned to guide and ensure tangible impact. By taking equity at an early stage, lead VCs sit on the board of their portfolio companies, allowing them to observe the impact trajectory of the startup. VCs are also able to lend their expertise to ensure SMEs have the best chance of succeeding, both as a business and as a changemaker. In companies that do not have an explicit impact agenda, VCs can still influence company direction and monitor indicators in the same way as larger asset managers. Some VCs even go as far as to explicitly include ‘sustainability clauses’ in term sheets, calling on firms to “regularly measure their carbon footprints, implement carbon offset schemes and promote environmental responsibility when engaging with customers and suppliers.”, as reported by CNBC.[75]

Impact related venture capital investments are not new – between 2006 to 2011, $25 billion was invested by Silicon Valley VCs into cleantech startups, aimed at reforming the energy sector. However, these bets did not pay off and failure rates were high, contributing to low IRRs and poor risk/return profiles, with almost half of the invested amount being lost.[76]

However, we believe that the developments over the past 10 years make it the right time to start rethinking about impact investments now. A concerted global movement across governments, businesses, individuals and the financial services industries have created the right policy environment and corporate demand for new green/sustainable solutions to flourish.

The level of technology today far outstrips that of the start of the millennium, which has opened up many opportunities for technological innovation in various verticals. There are many new applications (AI, blockchain, etc.) that can simultaneously disrupt and greenify industries. Analysis done by PwC and Microsoft show that applying AI alone in 4 sectors of the economy has the potential to eliminate 2.4 gigatons of global CO2 emissions in 2030, a clear sign of the potential that lies ahead.[77]

Green investments today are no longer limited to the energy sector, but also include any technology that helps to decarbonise the economy (broadly termed as climate tech, including energy, smart cities, smart mobility etc.). Impact investors are also increasingly looking at other verticals such as fintech and agritech, that can help to improve social conditions and achieve sustainability.

Additionally, we can learn from the failures between 2006 to 2011 to refine our criteria for seeking out the companies that are more likely to succeed. In order for start-ups with a sustainability objective to achieve the IRR needed for venture capital investing, it goes without saying that they have to be evaluated stringently.

With early stage investments, venture capitalists need to be discerning in selecting the right start-ups. The right fund manager will ask the right questions when assessing startups for feasible business ventures and substantial impact outcomes before making a decision with confidence. For example:

What level of impact value can potentially come from this business?

At Quest Ventures, we believe that outcomes for individual companies are measurable. We do so via the Logical Framework Approach (LFA), which is further expounded on, along with other impact investing frameworks for early stage venture capital in our previous publication.[78] Keeping the end in mind, the company can be assessed Focusing on a particular part of the value chain that can create the most impact?

Other considerations also include:

- How scalable and replicable is this business model across the region?

- What is the path to profitability?

- Will large amounts of upfront capital be required to prove the model?

- Is this the most effective solution to solve this particular problem?

Research done by PwC has stated that VC investment into climate tech is rising again, from $418 million per annum in 2013 to $16.3 billion in 2019, backing up our belief that there is an increasing amount of sound business opportunities that are capital efficient, create substantial & tangible ESG value and are technically feasible, making them suitable for venture investment.[79]

Trends and Developments I

There are several spaces that we have identified and are keeping an eye on. Below we provide a high-level overview of each particular industry, focusing on upcoming technology, as well as innovative business models.

Energy

Given the increasing public awareness of the need for cleaner energy and the efforts by governments to encourage a phasing-in of clean/sustainable energy sources, it is inevitable that we will see the toppling of the oil & gas era soon. These winds of change also mean that the energy sector’s landscape has morphed considerably since the early 2000s.

Today, solar and wind power technologies are well-proven and established, but still require additional innovations to provide a set of solutions that can rival and beat fossil fuels. Notably, there will need to be improvements in battery development, which is critical to overcoming the intermittent nature of renewable energy sources and reducing reliance on nature. In order to transition smoothly from fossil fuels, there also needs to be continued innovation in reducing emissions in electronics and supporting the spread of renewable energy (load-balancing and supply-demand balancing mechanisms). Lastly, the energy sector needs to continue to refine emerging technologies such as hydrogen fuel cells and biofuels.

Achieving sustainability for the environment in the energy sector would be a smooth and accelerated transition to a zero-emission economy, globally and regionally. This can be measured via increasing the penetration of renewables and declining carbon emissions. On a social scale, impact for sustainability can be measured by bringing affordable and environmentally friendly electricity to communities that are off-the-grid and relying on damaging fuel sources such as coal and kerosene.

Renewable Energy Generation

Besides solar and wind energy, the other forms of renewable energy that are often brought up are nuclear, geothermal and hydro power. We are bearish towards these forms of renewable energy for several reasons.

Nuclear power is still risky, as evidenced by the various incidents, and there is the real possibility of societal and political backlash from the risks as well as the potential ecosystem & environmental damage that arises from the radioactive waste produced. Nuclear plants require large capital expenses to build and maintain. With safer, cheaper and equally viable alternatives in solar and wind energy, there is no strong reason for ASEAN countries to overtly support or implement nuclear power. There is also a long way to go before safer nuclear fusion technology becomes a reality. According to Dealroom data, VCs have steered clear of nuclear generation focused start-ups, similar to Quest Ventures’ position.[80]

Likewise, geothermal and hydro power are also limited in where they can be applied across the region, and will require much more R&D and capital investment over a longer horizon before becoming commercially viable and/or see widespread adoption.

While it will be interesting to see how and where these three forms of renewable energy will come into play in the future, we expect that the renewable energy will continue to mainly come from solar or wind power.

Energy Storage

Lithium-ion batteries are the de-facto option for energy storage today. In recent years, they have been heavily used as part of electric vehicles (EVs), and in renewable energy-powered power grids and solar/wind farms. However, there are several issues with the existing lithium-ion battery technology that are limiting its applications.

Firstly, their energy density is still inferior to fossil fuels. Fossil fuels remain more convenient and efficient – a fully charged battery in an EV will not allow one to travel as far as a full tank of petrol, and will likely weigh more as well. Batteries are also limited in terms of how well they can hold their charge over periods of time. This limits the applications of batteries to small electronics such as drones and smartphones, or electric cars and electric trucks at best. While inventions such as commercial electric planes would reduce air travel costs and emissions significantly, they regrettably remain unachievable.

Even the most advanced lithium ion batteries today contain 14 times less usable energy than jet fuel, and a plane cannot possibly carry the weight of X such batteries to make up for the difference in energy density.[81] According to a study, batteries would need to be 4x as energy dense as the most advanced lithium ion batteries today before they can power a commercial airplane for ~1000km.[82]

Secondly, battery costs remain high. Battery costs are measured in terms of the amount of money spent for every kilowatt-hour of electricity the battery can hold. While lithium ion battery costs have fallen from $1000/kWh to $200/kWh from 2010 to 2017, further reductions must be made in the next decade.[83] The US Department of Energy estimates that battery costs will need to fall to $125/kWh in order for EV ownership to rival gas-powered car ownership, and for renewable energy power grids to replace traditional grids, battery costs will have to fall even further to $10/kWh.[84] Besides costly production, batteries have a limited lifespan and will require replacements after a particular number of charge cycles. This adds additional cost considerations that will detract from adoption of renewable energy solutions.

Thirdly, lithium-ion batteries use rare metals such as lithium, nickel, manganese and cobalt as key materials. Besides being only found in small quantities, they are often mined in countries with dubious labor and environmental regulations, such as the Democratic Republic of Congo.

There have been some noteworthy developments coming from start-ups across the world aimed at tackling these limitations.

The overall battery’s energy density can be increased theoretically by increasing the energy density of either the cathode, anode or both. The most promising cathode appears to be the lithium nickel-manganese-cobalt (NMC) 811 cathodes (the numbers refer to the ratios of the respective metals). However, more innovation needs to be done to increase its short lifespan. While most batteries have relied on graphite as the anode, materials such as silicon and lithium are being considered as potential better alternatives. Silicon anode technology is being used by start-ups such Silanano, and companies like Daimler and BMW have expressed their interest. Some startups are even looking at producing silicon sustainably (e.g. produced from barley husk ash or sand).[85] Other startups and researchers have also proposed alternative batteries, such as graphene batteries, lithium-sulfur batteries, solid-state lithium-ion batteries, gold nanowire batteries, sodium-ion batteries etc.[86] Each of these technologies has the potential to rival lithium-ion batteries in the next decade.

In the pursuit of sustainability, we are also seeing technology being applied by startups to search for rare metal deposits where extraction causes less negative externalities.[88] For example, Kobold is deploying AI to search for cobalt in places around the world with better environmental and labour regulations, while Deep Green is exploring deep-sea mining. Additionally, start-ups are pioneering new battery technology, utilising common metals and even materials like cotton to create batteries that can be used in small electronics and EVs. Audi and Umicore research and testing has shown that 95% of rare metals can be recycled.[89] Start-ups are now trying to find innovative ways to both improve this figure and ensure recycling’s cost-effectiveness. Lastly, start-ups are also trying to commercialise systems to recover rare metals lost during production processes.[90] Proper sourcing and recycling will help to conserve finite resources while the search for better long-term solutions is ongoing.

New types of batteries, cheaper raw materials as a result of better sourcing, different materials being used or the circular economy are all ways of successfully bringing down production costs.

With many interesting and novel technologies being developed, the energy storage vertical is one of the most interesting ones to watch out for within the energy sector itself.

Alternative Fuels – Hydrogen

Hydrogen is the most abundant element on Earth. It can be obtained through water electrolysis (splitting of water into hydrogen and oxygen via electric currents), fermentation of biomass feedstock, or through natural gas reforming.[91, 92] The resulting hydrogen can then be used to release energy on recombination with oxygen, with water as a byproduct. This makes hydrogen one of the cleanest energy sources available, when electrolysis is done with renewable electricity (termed as green hydrogen).

Hydrogen fuel cells are seen as a viable alternative to electric batteries. Applications such as hydrogen vehicles are being developed in tandem with EVs, and research suggests that green hydrogen will bring life-cycle emissions of vehicles lower than that of EVs, because of the current environmental costs of lithium-ion battery production.[93]

Nevertheless, the technology remains more of a niche than electric vehicles, due to limitations in infrastructure (hydrogen refuelling stations) and efficiency. However, innovative methods of electrolysis (e.g. photobiological, photoelectrochemical water splitting) and innovations in fuel cell technology could both supplement and supplant the dominance of batteries in electric powered transportation, especially in larger vehicles hampered by battery capacity.

Alternative Fuels – Biofuels

Biofuels can be divided into three generations. The first generation of biofuels were made from food crops, which meant that it’s sustainability and ethicality was immediately called into question. The second generation of biofuels, which we are currently using, are made from damaged or waste grain, forestry waste or even household waste. The third generation of biofuels will be the ones that are fully synthetic, but those are a long way off from achieving commercial success.

In ASEAN, we expect biofuels to grow in importance for several reasons. Firstly, growing certain crops for biofuels is a part of the rural development strategy for countries that retain a large agricultural base, such as Indonesia, Philippines and Thailand. As food production expands due to increased farm productivity, there is more waste grain and residues from harvests that can be used as feedstock for biofuel production.[94] This provides an additional source of rural income opportunities, aiding in the reduction of poverty for rural communities. In fact, growing non-food crops in rotation with existing crops can provide synergistic properties such as mutually fertilising the soil for each subsequent season and maximising land use during off-seasons.[95] This also applies to the forest plantations found all over Southeast Asia, and the communities formed around them. As such, there is incentive for several governments to get involved in promoting biofuel adoption. We are already seeing in the form of biofuel mandates, such as Malaysia’s attempt to support its palm oil industry. Singapore’s Economic Development Board (EDB) is also carrying out a study to determine if materials such as palm oil, sugarcane and plant biomass can be used to produce fuels, chemicals and polymers.[96]

Secondly, biofuels present a solution for countries to reduce their global carbon emissions quickly, as they often require little modification before usage. According to research by the International Renewable Energy Agency (IRENA), biofuels could potentially sustain up to two-fifths of the region’s projected transport fuel requirements by 2050, achieving considerable carbon emissions reductions and contributing to the energy security of each country.[97]

We are already seeing interesting movements made by start-ups in the area. Alpha Biofuels, a Singapore company, is converting used cooking oil into biodiesel, successfully using it in a bulk carrier.[98] The biggest challenge will be creating efficient fuels while balancing land use biofuel crop growth against other priorities. Hence, we can expect innovation to continue not just in the refining process and application of biofuels, but also in the agritech space to improve yield efficiencies of crops and hence residual biomass feedstock.

Grid Management

Increasing access to electricity and bringing communities on to the grid is one of the sustainable development goals. Aided by the decreasing capital costs of solar panels and turbines and small power grids, start-ups have married impact with business opportunities by providing electricity to rural households through pay-as-you-go or lease-to-own models. This is currently being done throughout Southeast Asia, in Myanmar, Indonesia, Philippines and Thailand, and has the added bonus of reducing usage of environmentally unfriendly sources such as kerosene and charcoal.

Looking Beyond

Evidently, there is still all to play for in the energy sector, and whichever companies can best balance safety and efficiency to come up with the best solutions can potentially see themselves becoming the Shell or Exxon of the electric era. The energy sector also parallels other sectors dealing with essential resources, such as water and air, where the challenge lies in Increasing accessibility to safe sources of essential resources at an affordable cost.

Trends and Developments II

There are several spaces that we have identified and are keeping an eye on. Below we provide a high-level overview of each particular industry, focusing on upcoming technology, as well as innovative business models.

Infrastructure

According to the UN, the world population will be approximately 9 billion by 2050, of which almost 66% will be living in cities.[99] This places great strain on existing infrastructure, as well as the environment. It is imperative that governments take the necessary steps to mitigate these challenges now. Naturally, this also provides the private sector with the opportunity to step in with solutions.

Smart Mobility

In sprawling urban jungles, getting from one place to another quickly is important for both life and work. This makes the development of efficient yet sustainable public and private transport options critical to the productivity of the country.

With regards to public transport, we are seeing constant improvement on train and bus services. In Singapore, rail operators have implemented technology such as re-using energy from braking trains to power up other trains, and are looking at lighter trains and recyclable parts.[100] Efforts are also being undertaken by start-ups across ASEAN to provide cleaner public transport options. This include hardware options such as buses running entirely on biogas, or using AI & user apps to introduce dynamic routing & buspooling (e.g. Rushowl in Singapore, Bussr in Indonesia). The end goal we should be working towards is a rail system like Sweden’s, which runs entirely on renewable energy. To continue pushing public transport (trains, buses, bicycles etc.) as a viable alternative to private transport, ASEAN governments need to continue their commitments to building the necessary infrastructure.

We are seeing an increase in the availability of hybrid vehicles and EVs in ASEAN. Nissan recently announced in 2021 that Thailand would be its EV hub for the region, and startups across ASEAN have sprung up to produce their own EVs, electric bicycles, scooters etc. Similarly, infrastructure investments and government regulation will be key towards advancing the adoption of EVs. Thankfully, we have seen the Singaporean, Thai, Indonesian and Philippines governments commit to building this infrastructure. Singapore aims to install 60,000 charging points by 2030, and the Asian Development Bank (ADB) has signed a green loan to Energy Absolute in Thailand to finance a EV charging network.[101, 102] We are also seeing subsidies for electric vehicle ownership, including the reduction of road taxes on the basis of reduced carbon emissions, and stricter requirements on models that are allowed to be distributed or even driven within countries.

We are also seeing the proliferation of tech-based mobility solutions that are disrupting traditional notions of private hire vehicles and private car ownership. This includes the now well-known model of ride-hailing (e.g. Grab, Uber, Gojek, Ola, Lyft, Didi etc.), as well as ride-sharing (e.g. Grabhitch). We are also seeing the proliferation and expansion of car-sharing mobility startups such as BlueSG (Singapore), SoCar (South Korea) within Southeast Asia. Micro-mobility is also a plausible trend to look out for. While we have seen the rise and less than glamorous fall of bike-sharing start-ups such as Ofo, oBike and Mobike, the micro-mobility scene today is looking towards electric scooters as the next last-mile mobility solution.[103] With the operational and regulatory lessons learnt from bike-sharing, e-scooter sharing might be able to succeed where bike-sharing failed.[104] Lastly, the parking and navigation space is also seeing several start-ups attempt to use AI and blockchain technology to solve congestion, parking inefficiencies and other pain points.

Smart Logistics

The pandemic has heightened demand for online purchases and highlighted the inefficiencies in the current processes and systems. There is room for AI and technology to bring about coordination, efficiency and optimization to the fragmented logistics network. By offering SaaS or in-house solutions, start-ups may potentially find success in a region where logistics and shipping continues to be a large industry. We are also seeing new fringe applications aimed at revolutionising last-mile logistics solutions, such as drone delivery.

Smart Buildings

Being geographically positioned near the equator, tropical countries in Southeast Asia are some of the hottest all-year round. Additionally, Asian cities are some of the most densely populated, characterised by high-rise living and congestion. High population density, together with intense human activity and energy consumption synonymous with urban living environments has resulted in what is known today as the urban heat island (UHI) phenomenon. High temperatures in turn spur citizens to rely on air conditioning to create artificially cool indoors environments conducive for work, which consume large quantities of electricity from the grid, creating a large carbon footprint while venting hot air outdoors, raising the temperatures further. Heat stress is expected to cost APAC 62 million full-time jobs by 2030, or 3.1% of the workforce, according to the International Labour Organization, thus it is imperative that future urban planning and development aim to mitigate rising temperatures.[105]

We should be looking towards constructing or converting existing buildings into green buildings. These are buildings that use innovative architectural designs or inventions to achieve sustainability. Countries assess green buildings via rating schemes, such as the Singapore Building Construction Authority (BCA)’s Green Mark rating scheme and their counterparts in Malaysia & Indonesia etc.[106] These are attuned to the regional context, focusing on passive: and active: technologies that can promote cooler buildings while reducing energy consumption.[107, 108]

Examples of technologies include:[109]

- Design innovation led by modelling software to optimise shade and ventilation

- Architectural designs like overhangs, planters to block direct solar exposure, roof greening and facades

- Efficient cooling systems such as water cooling for data centers

- Motion sensors and intelligent building control systems that regulate electricity use based on activity/outside temperature

- Solar windows and cool roofs, paints that reflect sunlight and prevent absorbing heat

- Sustainable construction materials with less embodied carbon

Governments are increasingly launching grants for green building technologies, and start-ups can take advantage of these to get their innovations ready for commercialization and further funding.

Smart appliances are also continuously being developed, and continued innovation will serve to make them more energy efficient and lower costs, thus driving adoption. Homes are a main contributor to energy consumption as well, and establishing zero-energy homes will be an important goal for cities as well.

Trends and Developments III

There are several spaces that we have identified and are keeping an eye on. Below we provide a high-level overview of each particular industry, focusing on upcoming technology, as well as innovative business models.

Agriculture

Agriculture remains one of the most vital sectors of most ASEAN economies. Research done shows that agriculture (including farming, fishing and forestry) continues to account for 10.2% of ASEAN’s total GDP as of 2019, and remains a key contributor to employment both in developing countries such as Myanmar (almost 50%), Laos, Vietnam and Thailand, as well as countries that are rapidly pivoting to industry and service sectors such as Indonesia and the Philippines.[110] When considering the agriculture value chain as a whole, the value created is multiplied (2.9x in the Philippines), increasing agriculture’s importance to economies as a whole.[111]

Furthermore, with the global population set to reach 10 billion by 2050, agricultural production needs to double in order to provide sufficient food for all. More efficient and sustainable agriculture will be integral in meeting these needs without infringing further on the environment. Simply scaling up will place unprecedented levels of strain, resulting in groundwater depletion, soil degradation, loss of biodiversity amongst other climate stresses. There is a need for fragmented supply chains to become more unified and efficient, for land to be used more efficiently and for alternative foods to be developed and adopted.

Efficiency

We have already seen an agricultural revolution in the form of hardware improvements. Today, we are seeing the rise of precision farming, where softwares such as GPS, AI & data analytics, IoT and cloud computing are used alongside hardware (sensors, machines, drones etc.) to provide farmers with the tools to monitor, anticipate and tackle challenges. This allows for improvements in crop yields and stabilizing of harvest levels to ensure food security.